Thoughtful renovation decisions can significantly influence both a property’s financial value and the overall experience of living in it. Many homeowners approach remodelling projects with aesthetics in mind, but effective home renovation strategies require balancing visual improvements with practical upgrades that align with market expectations. When renovations are planned strategically, they can improve functionality and increase property value and buyer appeal.

For homeowners considering upgrades, it is helpful to consult a realtor for home modifications that increase value before beginning major projects. Real estate professionals can offer insight into local market preferences, neighbourhood standards, and the types of upgrades that resonate most with buyers. While renovation decisions ultimately remain personal, understanding how certain changes affect resale potential helps homeowners prioritize improvements that deliver lasting value.

Not every renovation provides the same financial return. Some upgrades focus on maintenance and preservation, while others aim to modernize a property or expand usable space. Recognizing this distinction allows homeowners to use strategies that improve daily comfort while also protecting long-term investment.

Understanding Renovation Types: Maintenance vs. Strategic Upgrades

A key step in renovation planning is recognizing the difference between essential maintenance work and improvements designed to increase property value. Both play important roles in responsible homeownership, but they serve different purposes.

Maintenance projects focus on preserving the home’s structure and preventing deterioration. Strategic renovations, on the other hand, are intended to modernize the property, enhance functionality, and strengthen the property’s market competitiveness.

Necessary Maintenance That Protects Property Value

Maintenance upgrades do not always produce immediate financial returns, but they are essential for maintaining buyer confidence. Neglected repairs can reduce perceived value and create concerns during inspections.

Common maintenance improvements include:

- Roof repairs or replacement when materials reach the end of their lifespan

- HVAC servicing or system replacement for aging equipment

- Plumbing or electrical updates to meet modern safety standards

- Foundation stabilization or structural reinforcement

While these projects may not dramatically transform a home’s appearance, they support responsible home renovation strategies by protecting structural integrity and preventing future issues that could affect resale.

Strategic Renovations That Increase Property Value

Strategic upgrades focus on areas of the home that influence buyer decision-making. These improvements modernize the property and align it with current design expectations.

High-impact renovations comprise:

- Kitchen refreshes such as cabinet refacing, countertop upgrades, or modern appliances

- Bathroom remodels with updated fixtures, improved lighting, and improved storage

- Flooring replacement that creates visual consistency throughout the home

- Energy-efficient window installation or insulation improvements

When planned carefully, these projects can simultaneously improve everyday living, increase property value, and enhance buyer appeal.

Planning Renovations with Market Awareness

Every neighbourhood develops its own pricing range and design expectations. Renovations that align with these standards are more likely to produce positive returns.

Homeowners consider working with a realtor for home modifications before undertaking extensive changes. Market knowledge helps determine:

- Which upgrades buyers currently prioritize

- Whether certain renovations may exceed neighbourhood expectations

- How renovation budgets compare with potential resale gains

Consulting market insight early can guide renovation planning toward projects that strengthen long-term investment value.

High-Impact Home Renovation Strategies That Attract Buyers

Certain areas of the home consistently influence buyer interest and property valuation. Improvements that address these spaces produce the strongest results when attempting to increase property value and buyer appeal.

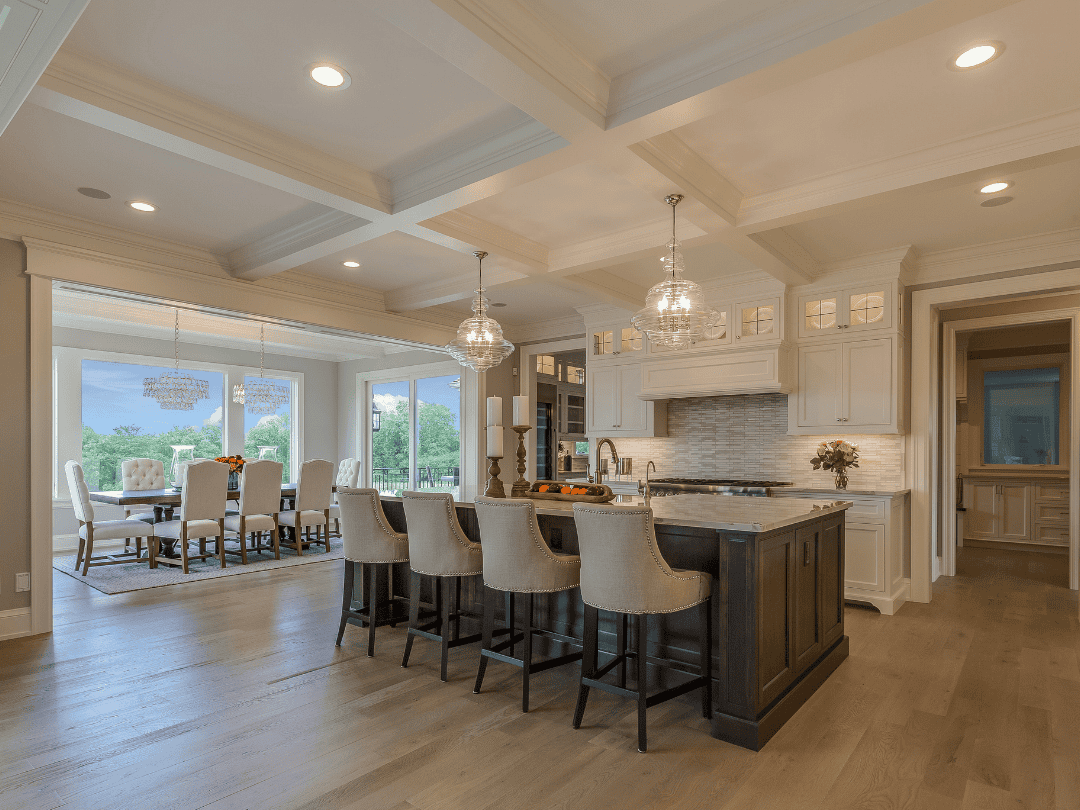

Kitchen and Bathroom Improvements

Kitchens and bathrooms are often considered the most influential interior spaces during property evaluations. Buyers typically assess these areas closely because they are both highly visible and expensive to renovate.

The following are effective kitchen and bathroom upgrades:

- Replacing outdated countertops with durable materials

- Updating cabinet hardware or refacing existing cabinetry

- Installing modern lighting to improve brightness and atmosphere

- Upgrading plumbing fixtures for efficiency and contemporary design

- Improving ventilation and moisture control

These improvements allow homeowners to implement practical home renovation strategies that modernize the home without requiring a full structural remodel.

Energy Efficiency and Lighting Upgrades

Energy-efficient improvements have become an increasingly important component of renovation planning. Homeowners and buyers alike recognize the long-term benefits of reduced energy consumption and lower operating costs.

Examples of efficiency-focused renovations are:

- LED lighting conversions throughout the home

- Smart thermostats and improved HVAC efficiency

- Insulation upgrades in attics and walls

- Energy-efficient windows or doors

These upgrades contribute to comfortable living conditions while also helping increase property value in markets where sustainability and utility savings are becoming priorities.

Curb Appeal and Exterior Improvements

Exterior improvements play a major role in shaping buyer perceptions. First impressions are formed before potential buyers even step inside the property.

Here are exterior renovation ideas that help enhance buyer appeal:

- Updated entry doors or garage doors

- Fresh exterior paint or siding improvements

- Landscaping upgrades that improve visual presentation

- Outdoor lighting and walkway enhancements

- Patio or deck additions that extend living space

In fact, recent renovation data shows that exterior projects deliver some of the strongest returns. For instance, garage door replacement has been reported to achieve an average return on investment of approximately 194%, making it one of the highest-value renovation projects in North America. These results highlight why exterior improvements are frequently included among effective home renovation strategies designed to improve resale potential.

Avoiding Renovation Mistakes That Reduce Resale Value

While renovations can significantly strengthen a property’s value, certain choices may unintentionally limit buyer interest. Successful planning requires balancing personal preferences with broad market appeal.

Over-improving the home relative to surrounding properties is one common issue. If renovation costs exceed what the neighbourhood market supports, homeowners may struggle to recover those expenses at resale.

Other factors that can reduce buyer interest:

- Highly personalized design features that appeal only to niche tastes

- Unusual room conversions that reduce functionality

- Removing storage space or bedrooms

- Excessively luxurious finishes in modest neighbourhoods

Neutral design choices produce stronger results when the goal is to increase property value. Buyers generally prefer homes that let them imagine their own style rather than adapt to highly customized interiors.

Another overlooked consideration is the balance between renovation costs and expected returns. Not every improvement will recoup its full cost, so homeowners often focus on upgrades that simultaneously enhance daily living and maintain competitive resale value.

This is why many homeowners choose to consult a realtor for home modifications that increase value. Market knowledge helps ensure renovations and upgrades align with buyer expectations and neighbourhood standards.

Balancing Personal Upgrades With Market-Focused Renovation Decisions

Home improvements can transform both the comfort and financial potential of a property. When approached thoughtfully, home renovation strategies allow homeowners to modernize their living spaces while protecting long-term investment value. Strategic upgrades to kitchens, bathrooms, flooring, lighting, and outdoor areas can help increase property value and buyer appeal.

At the same time, successful renovation planning requires awareness of local market conditions, buyer expectations, and neighbourhood standards. Improvements that balance functionality, visual appeal, and cost efficiency produce the most sustainable results.

Before committing to significant upgrades, many homeowners find it beneficial to seek professional market insight. In many situations, it is best to consult a realtor for home modifications that increase value. This way, renovation decisions reflect realistic market trends, buyer preferences, and long-term resale considerations.